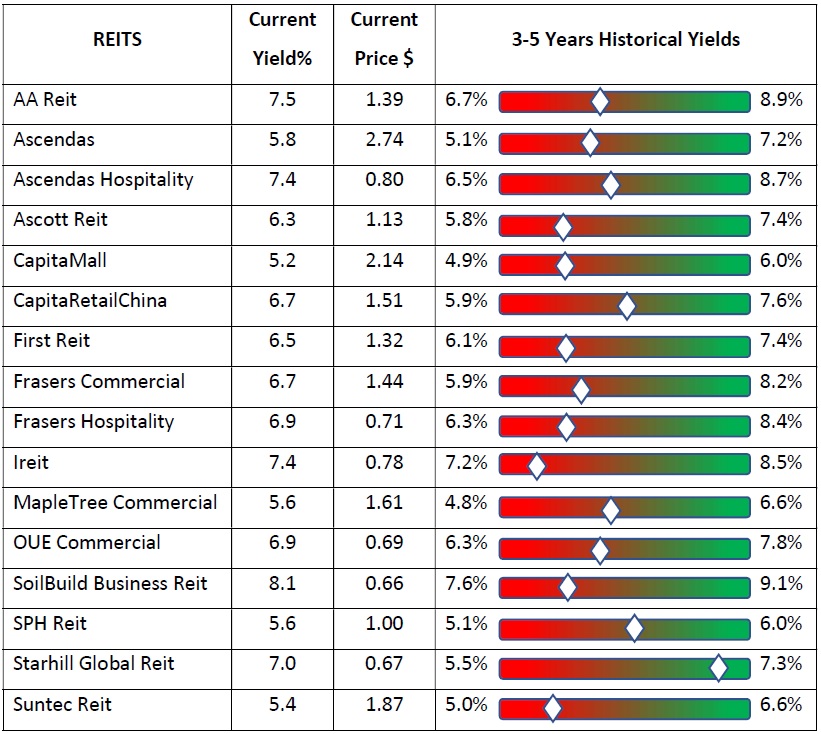

At the bottom of this post is a chart that I have made to show where the current yield of some of the SReits lies on the spectrum of their past 3-5 years historical yields.

Although most of the SReits are off their recent highs, their current yields are still within the lower half of the spectrum. (In order to read this, we need to appreciate that High Price means Low Yield and vice versa, assuming same DPS).

Just to quote some examples,

- Ascendas – 5.8% current yield, 35% on the spectrum (0%-lowest yield (5.1%)and 100%-highest historical yield(7.2%))

- CapitaMall – 5.2% current yield, 31%

- OUE Commercial – 6.9% current yield, 43%

- Suntec Reit – 5.4% current yield, 22%

Among the SReits that I researched on, only SPH Reit and Starhill Global are on the upper half of spectrum, with CapitaRetailChina coming close to the 50% mark.

As some of you know, I am a believer of reversion to mean, especially when it comes to Reits. This is because the Reit business model is fixed and the dividend payout from cash is fixed within a tight range (90-100%). When they only have the mandate to invest in certain types of properties and in specific geography, then in some ways, their risk profile is defined. Hence, we often see Reits that are investing in the same type of industry tend to bunch up around a certain dividend yield range.

Hence, if we believe this, then by theory, the yield will return to the mean/average yield if there is no internal and/or external stimulant or depressant.

There is a good chance that Starhill Global’s dividend yield will eventually move down to the mean yield (i.e. share price will move up) since there is no major change internally within its company and externally with the business environment. Mr Market is probably too pessimistic with the challenges posed by e-retailers at the moment.

Assuming the same DPS, for the yield to move back to mean/average, the share price will rise to 72.5 cents … not a bad deal, quite a handsome gain from the current share price of 66.5 cents.

(To add on a sweetener, the net asset value of Starhill is 92 cents, so we will be buying at about 20% discount if we pay 72.5 cents)

Personally, I will wait for their latest results and see what is the amount of dividend declared and if there is no significant (negative) surprises, I will start accumulating Starhill again.

I used the term “again” because as per my earlier blog, I already did some accumulation of Starhill a while back (see references below) when it’s price started to fall to my “buy” level. Unfortunately, the price continued to decline further. I got worried and so I stopped. I was concerned whether there is something adverse about the company that I was not aware of. Now that things are starting to get stable again for Starhill, I am gaining confidence to start accumulating again after everything is okay.

Based on the analysis below too, I won’t be adding more SReit (except Starhill) to my portfolio for the moment.

Hope you find this useful and have a great weekend.

Regards, Warriortan

References:

Hi Warriortan,

May I know how you get the historical high and low dividend yield? Is it from Bloomberg terminal

Thanks.

Incomeinvestor

LikeLiked by 1 person

From annual reports

LikeLike

I used the annual dividend distribution and get the yields from highest and lowest share price for the year.

LikeLike